Make your 2X MATCHED gift today!

This week only: Every $1 will be matched with $2 to enable women worldwide.

This week only: Every $1 will be matched with $2 to enable women worldwide.

Posted on 08/15/2022

I learned of the work of Muhammad Yunus, the founder of the Grameen Bank, decades ago, when I was on the board of a San Francisco Bay Area nonprofit organization which specialized in empowering disadvantaged immigrant women by training and transferring business skills to them.

While at Wells Fargo Bank prior to my retirement, I learned of the program Bankers without Borders under the same Grameen umbrella, and had always wanted to get involved in volunteer work sponsored by this organization. In early 2020, after having retired from the bank for a couple of years, I was offered the opportunity to participate in an on-the-ground volunteer project in the Farmer to Farmer program as part of the Bankers without Borders efforts in the Philippines. The project involved helping with the improvement of the loan repayment process of Laak Multi-Purpose Cooperative (LAMPCO), an agricultural multipurpose cooperative that promotes the integration of economic activities such as providing credit to its members. I was most excited with the opportunity and was prepared to go to the Philippines in May of 2020. Of course, normal life as we knew it came to a grinding halt in spring of 2020. With the global disaster of the coronavirus pandemic, I regrettably had to pull out of this volunteer opportunity.

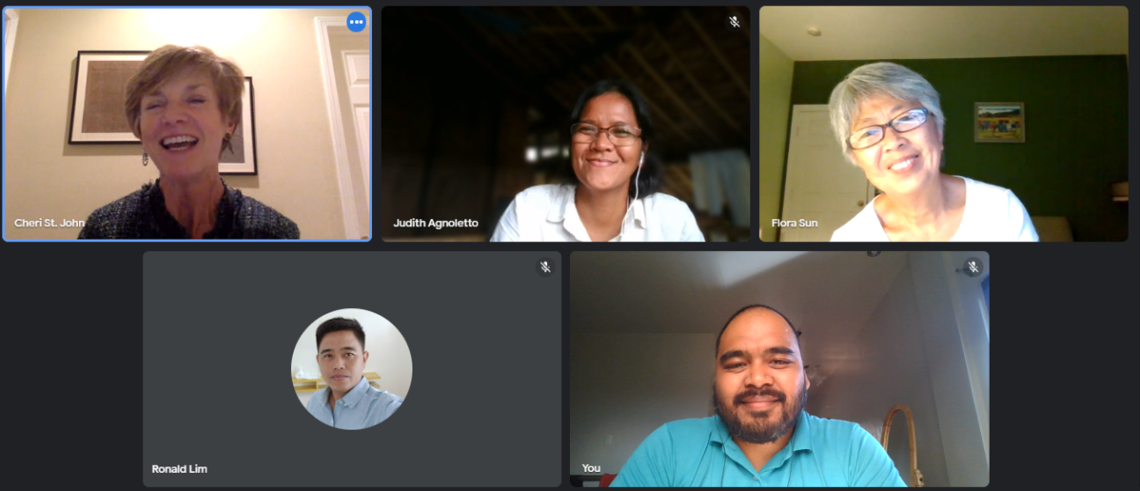

In the fall of 2021, I became re-engaged with the Farmer to Farmer (F2F) COCOS team when they reached out to me regarding another project opportunity with LAMPCO; this time for the implementation and training of a Credit Scorecard for the reduction of the portfolio loan default rates. Having come from the banking industry where I did work on credit analytics using scoring for credit risk control, I thought it would be a good fit. However, in examining the Statement of Work (SOW), I decided that there was a likelihood that the project may require: 1) A thorough review of the proposed scorecard for implementation, and 2) A re-development of a simpler scorecard for LAMPCO. At that time, I decided that I would need to bring in the help of a scorecard expert, none other than my previous manager, Cheri St. John, from our Wells Fargo days, who was also the original developer of the early generations of the now ubiquitous FICO score. Cheri took an early retirement around the same time I did, and she graciously accepted the invitation to help with this worthwhile project.

With the unrelenting pandemic still largely looming, the scorecard project was to be developed and delivered remotely, with Cheri and I in the San Francisco Bay Area conducting Zoom calls with each other, as well as with the F2F and LAMPCO teams virtually. Early on in the project, Cheri and I decided that setting a weekly time on our calendar for touch-base Zoom calls would be most effective to project plan, map out milestones, jointly work on deliverables, and to prepare presentations for the LAMPCO team. We held semi-regular Zoom calls with the LAMPCO team, for information gathering, findings sharing, and development updates. This remote process was clearly not without challenges, but it worked sufficiently well for significant progress to be made according to the timeline agreed upon with all parties. The dedication of the LAMPCO team, especially Ma’am Edesa with her deep engagement in the assessments and development processes, and the diligence and attention provided by our interpreter Ronald Lim, we were able to jointly make the project a success.

The first part of the project was mostly data gathering and fact finding. With the help of the LAMPCO leads, we were able to assess their current state, which was primarily a loan portfolio with an unsustainably high default rate. We also received the existing scorecard they were hoping to implement, and upon our thorough review process, we deemed that the scorecard was more complex than what LAMPCO needs or is capable of implementing. We then met with the Grameen F2F team, and recommended that the SOW be redefined, with the re-development of a credit scorecard as the first priority of the project, and the training/implementation to come at a later stage. Our recommendations were accepted by both the F2F and LAMPCO teams and a new SOW was written.

With the new project goals in mind, we got to work with the LAMPCO team. The early Zoom calls with the team, as well as the comprehensive review of their detailed loan data which included previous loan applications, loan amortization schedules, and repayment performance, paved the foundation of the subsequent development work. At the time, the loan officers assessed the repayment capacity of the borrowers using the application data alone, without considering previous loans performance, nor did they include the incremental burden of the new loan payments. Cheri and I went to work after requesting, and receiving, the data of 60 loans: 30 non-performing and 30 paid-as-agreed. We ran analytics, and conducted statistical analyses, and were able to find ways to improve performance by building a new scorecard with a shorter list of characteristics including borrowers’ demographic data, assets, income and expenses. Most importantly, including the new loan debt burden helped to more accurately assess the borrowers’ capacity to repay. We shared our findings and recommendations with the LAMPCO team, with Ronald’s help in real time interpretation along the way.

Once the recommendations were accepted, we moved onto the pre-implementation part of the project. A credit scorecard is normally a highly quantitative tool, best deployed in an automated fashion, rather than hand calculated. We worked to develop a Calculator in Excel, whereby the loan officers can input the data, and the automated calculator would produce the respective score of the borrower. The score will help with the loan approval process by providing a credit risk assessment of the individual borrower. We recommended that LAMPCO implement the scorecard as a pilot for a 3-month period, and then review the results to determine the next steps of full implementation. We delivered the final scorecard and calculator in May, and then did a remote live training session on how to use the scorecard with the loan officers. With the new tool in their hands, we are hopeful that they are now empowered to make better credit decisions and reduce their portfolio risk.

The project lasted from November 2021 through May of 2022. It was rewarding to see the engagement of the LAMPCO team, from Ma’am Edesa to the loan officers, to the Board of Directors. Because we are still unable to travel, at least through next year, we will be relying on our F2F COCO partners to help guide and encourage the LAMPCO team to implement, monitor and evaluate the success of the scorecard implementation.

Cheri and I are privileged to have been given the opportunity to make a small difference in the improvement of LAMPCO’s portfolio quality. We hope our contributions are meaningful and will help set a revitalized and rigorous credit risk management practice at LAMPCO.